On the cash flow statement, accounts receivable appears in the operating activities section as a period-over-period change adjustment, not as a standalone line item. An increase in AR is subtracted from net income because cash was earned on paper but not yet collected. A decrease is added back because customers paid prior invoices, converting receivables into actual cash.

Key Takeaways

- Accounts receivable appears in the operating activities section of the cash flow statement as a line item called "Change in accounts receivable," not as a standalone balance.

- An increase in AR reduces operating cash flow; a decrease adds to it. The math is direct: if AR grows by $50,000 in a quarter, $50,000 is subtracted from net income on the cash flow statement.

- Under the indirect method: start with net income, subtract AR increases, and add AR decreases to arrive at net cash from operating activities.

- Businesses offering net 30, 60, or 90 terms can eliminate the cash flow drag by using a net terms financing platform that advances invoice value within 24 hours.

How accounts receivable appears on the cash flow statement

Accounts receivable does not appear as a standalone line item the way it does on the balance sheet. Instead, the change in AR between two periods shows up as an adjustment in the operating activities section.

- If AR increased during the period: subtract the difference from net income. Cash was earned on paper through credit sales but not yet collected.

- If AR decreased during the period: add the difference back to net income. Cash arrived from prior-period invoices.

This adjustment reconciles accrual-based net income with actual cash generated.

What is a cash flow statement?

A cash flow statement is a financial statement that highlights changes in assets, equity, and liability, charting the total change in use of cash during a given period. This reveals a business' liquidity and helps analyze a company's operating activities.

Also known as a statement of cash flows, this is one of the main reports in your financial statements documenting the total amount of cash and cash equivalents your business received and used during a specified period. Unlike an income statement, which can include non-cash revenue like accrued sales, the CFS focuses strictly on actual cash movement. For example, if you invoiced a customer for $15,000 this month but haven't collected the payment yet, that amount would appear on your income statement as revenue, but it wouldn't show up as a cash inflow on your CFS until the customer actually pays. This distinction is what makes the CFS such a critical tool for understanding your real financial position—especially if you're a B2B business that regularly extends net 30, 60, or 90 terms to customers.

Why businesses need cash flow statements

Besides acting as a bridge between the balance sheet and the income statement, there are at least five reasons why businesses need a cash flow statement:

1. It provides proof your business is on stable financial ground

A cash flow statement lets you prove to investors that your company has squeaky-clean financials. This helps you to gain more trust and build credibility with those buying into your business, and it helps you secure more funding so you can scale.

How do you prove your business' liquidity? That's where a CFS comes in handy. They show the exact position of your company's cash flow. For instance, imagine you're a wholesale distributor pitching to a venture capital firm. Your income statement might look great, but if your CFS reveals that most of your revenue is tied up in unpaid invoices with 90-day payment terms, investors will see a different picture. A well-prepared CFS demonstrates that you're not only generating revenue—you're actually collecting cash and managing your working capital responsibly.

2. It spotlights details on changes to assets, liabilities, and equity

A cash flow statement lets you and your investors deep dive into changes in assets, liabilities, and equity. This includes cash balance, cash inflows, and cash outflows. These three areas form the accounting equation, helping you measure business performance.

For example, suppose your accounts receivable jumped from $50,000 to $120,000 in a single quarter. That change shows up on the CFS as a reduction in operating cash flow—even though your sales grew. By highlighting these shifts, the CFS gives you a clear signal that your collection cycle may be stretching too long and that your AR management process needs attention before it starts eroding your liquidity.

3. It makes it easy to compare your financial performance with competitors

A cash flow statement makes it easier for investors to compare your business's performance to others. For instance, one firm might be using accrual basis accounting while another uses cash basis; CFS provides a level field that eliminates the effects of these different bookkeeping techniques.

This matters more than you might think. Two companies in the same industry can report identical revenue numbers on their income statements, yet have wildly different cash positions. The CFS strips away those accounting method differences and shows how much actual cash each business generated. If a competitor is reporting strong profits but consistently negative operating cash flow, that's a red flag for investors—and a potential competitive advantage for your business if your CFS tells a healthier story.

4. It helps you forecast cash flow

A CFS can help you predict future cash flows as you can create cash flow projections. You can do this by planning how much liquidity you expect in the future, which is vital for long-term business planning.

Say you're a manufacturer who routinely sells on net 60 terms. By reviewing your CFS over several quarters, you can identify seasonal patterns in when cash actually arrives versus when sales are booked. That insight lets you forecast slow-collection months and plan ahead—whether that means building a cash reserve, adjusting your cash flow management strategy, or using a net terms financing partner to bridge the gap.

5. It helps you secure more funding

The only way you can secure a loan or line of credit is by keeping your CFS up-to-date. Like investors, banks also want to see that you have positive cash flow.

Lenders typically examine your operating cash flow closely because it demonstrates whether your core business generates enough cash to cover debt repayments. If your CFS shows that you consistently collect more than you spend on operations, you become a lower-risk borrower. On the flip side, even a profitable business can be denied financing if its CFS reveals chronic collection problems or heavy reliance on accounts receivable financing to stay afloat. That's why keeping your CFS current and accurate isn't just good practice—it's a prerequisite for securing the capital you need to grow.

Positive cash flow vs. negative cash flow

When your CFS has a negative number, that means you lost money during that accounting period (for example, you spent more cash than you received). However, just because you have a negative number does not mean you need to panic.

A negative cash flow balance doesn't always spell doom and gloom. Sometimes you might decide to spend more cash than usual in the hope of future returns, such as investing in office equipment.

For instance, Netflix racked up negative cash flows for years as it increased spending to come up with compelling content against its competitors, with the gamble paying off handsomely.

Generally, positive cash flow indicates you have a healthy business. In the long run, it isn't always a cause for popping champagne. While it may mean the business is currently liquid, a positive cash flow may have been a result of taking out a loan to keep the business afloat.

The key takeaway here is context. A negative cash flow driven by strategic investment—such as purchasing new manufacturing equipment or expanding into a new market—is very different from a negative cash flow caused by customers consistently paying late. Understanding what's driving the number is more important than the number itself. If you find that late-paying customers are the primary cause, it may be time to revisit your invoice payment terms or explore solutions that accelerate collections.

Where do cash flow statements come from?

If you're starting out, you can do simple bookkeeping in Excel and use your income statement and balance sheet to help you calculate the CFS.

As your business grows, you can upgrade to more robust accounting practices by using the information entered in the general ledger to automate the CFS-making process using accounting software. Most modern platforms—QuickBooks, NetSuite, Xero—can generate a CFS automatically by pulling data from your general ledger entries. These tools reconcile your accounts receivable, accounts payable, depreciation, and other line items to produce all three sections of the CFS with minimal manual effort. For businesses that extend net terms, integrating your AR automation platform with your accounting software ensures that your CFS reflects real-time collection data rather than estimates.

How to calculate cash flow

There are two main methods of generally accepted accounting principles (GAAP) that can help you develop a CFS:

1. Direct method

The direct method refers to cash-basis accounting as you record every transaction whenever you receive or disburse cash, only bringing it up when preparing the CFS at the end of the month.

As you can tell, it takes more effort since you need to track every cash transaction, and then subtract cash flow from the inflow. That includes items such as cash receipts, interest received, and income tax payments. The upside is transparency—you get a line-by-line view of exactly where cash came from and where it went. For instance, you'd see a specific entry like "cash received from customers: $200,000" and "cash paid to suppliers: $85,000," giving stakeholders a straightforward picture of operating cash movements.

2. Indirect method

Small businesses prefer this method to track cash received and cash payments from the business. They can record transactions whenever they accrue, rather than when cash changes hands, a method known as accrual accounting.

Incidentally, that means you'd have to go back to the income statement to eliminate transactions that do not reflect cash transfers. It may seem tedious, but the upshot is you don't have to go back to reconcile your statements. Most small and mid-sized businesses choose the indirect method because their accounting software is already set up for accrual-based reporting. You start with your net income and then adjust for non-cash items like depreciation, and working capital changes like increases or decreases in accounts receivable and accounts payable.

Direct vs. indirect method: a quick comparison

| Feature | Direct Method | Indirect Method |

|---|---|---|

| Accounting basis | Cash-basis | Accrual-basis |

| Starting point | Individual cash receipts and payments | Net income from the income statement |

| Complexity | Higher — requires tracking every cash transaction | Lower — adjusts net income for non-cash items |

| Transparency | Shows exact cash sources and uses | Shows adjustments; less granular detail |

| GAAP compliance | Accepted (preferred by FASB) | Accepted (most widely used) |

| Best for | Businesses needing detailed cash visibility | Most SMBs using accrual accounting software |

| Reconciliation | Requires separate reconciliation to accrual records | Built into the adjustment process |

What's in a cash flow statement?

A CFS is different from the other financial statements, and there are three main sections to be aware of:

-

Cash flow from operations: This contains data on incoming cash from current assets and current liabilities, including all operational business activities such as salaries, and buying and selling inventory. It also captures changes in accounts receivable and accounts payable, making it the section most directly affected by your credit and collection policies. If your customers are slow to pay, this section will reflect it as a reduction in operating cash flow.

-

Cash flow from investing activities: This shows your investment losses and gains. An analyst can use this to work out the capital expenditure (CapEx) changes. For example, it includes transactions like mergers and acquisitions, or purchasing equipment. A manufacturing company buying a new production line for $500,000 would show that as a cash outflow here, even though the equipment is an asset that will generate returns over time.

-

Cash provided by financing activities: This is cash spent or earned through financing with loans, owner's equity, or lines of credit. Briefly, it reveals the cash flow between you, your business, and creditors from raising money from debt, stock, or debt amortization. After you're done with all the calculations, you will be left with a single metric: net cash flow.

The CFS may also include non-cash items such as obsolescence and depreciation expenses. Depreciation and amortization reduce net income in the income statement, although you add them back to the CFS as they are non-cash expenses.

Sidebar: Accounts receivable and account payable are nuanced in nature

It's tempting to label cash flow as 'cash in' or 'cash out,' but the way a business spends and receives its cash is more nuanced than that, necessitating the preparation of accounts receivable and accounts payable.

The effect of accounts payable on cash flow

When a company purchases supplies, it may not necessarily pay straight away. They may get an allowance of 30, 60, 90, or 120 days before the supplier requires a payment. The purchaser records this short-term liability as accounts payable on the balance sheet.

For the purchaser, that is akin to a source of cash as it increases cash flow and cash in hand. Think of it this way: if your supplier gives you net 60 terms on a $50,000 order of raw materials, you have that $50,000 available to use for other business operations during those 60 days. On your CFS, an increase in accounts payable shows up as a positive adjustment to operating cash flow because it represents cash you haven't had to spend yet.

Although providing longer payment options can harm your cash flow, what if we told you there is a solution that allows you to do that without harming cash flow?

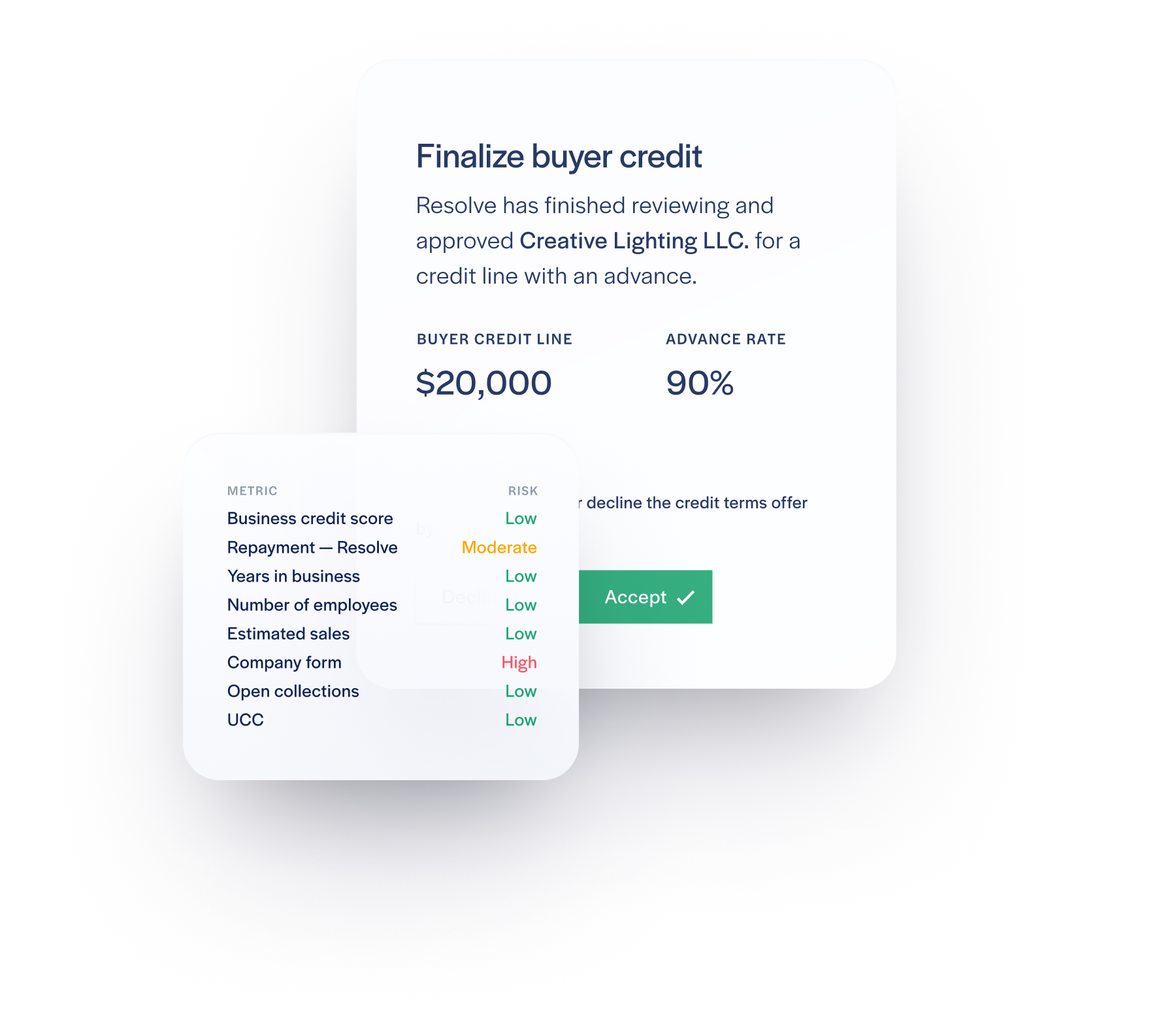

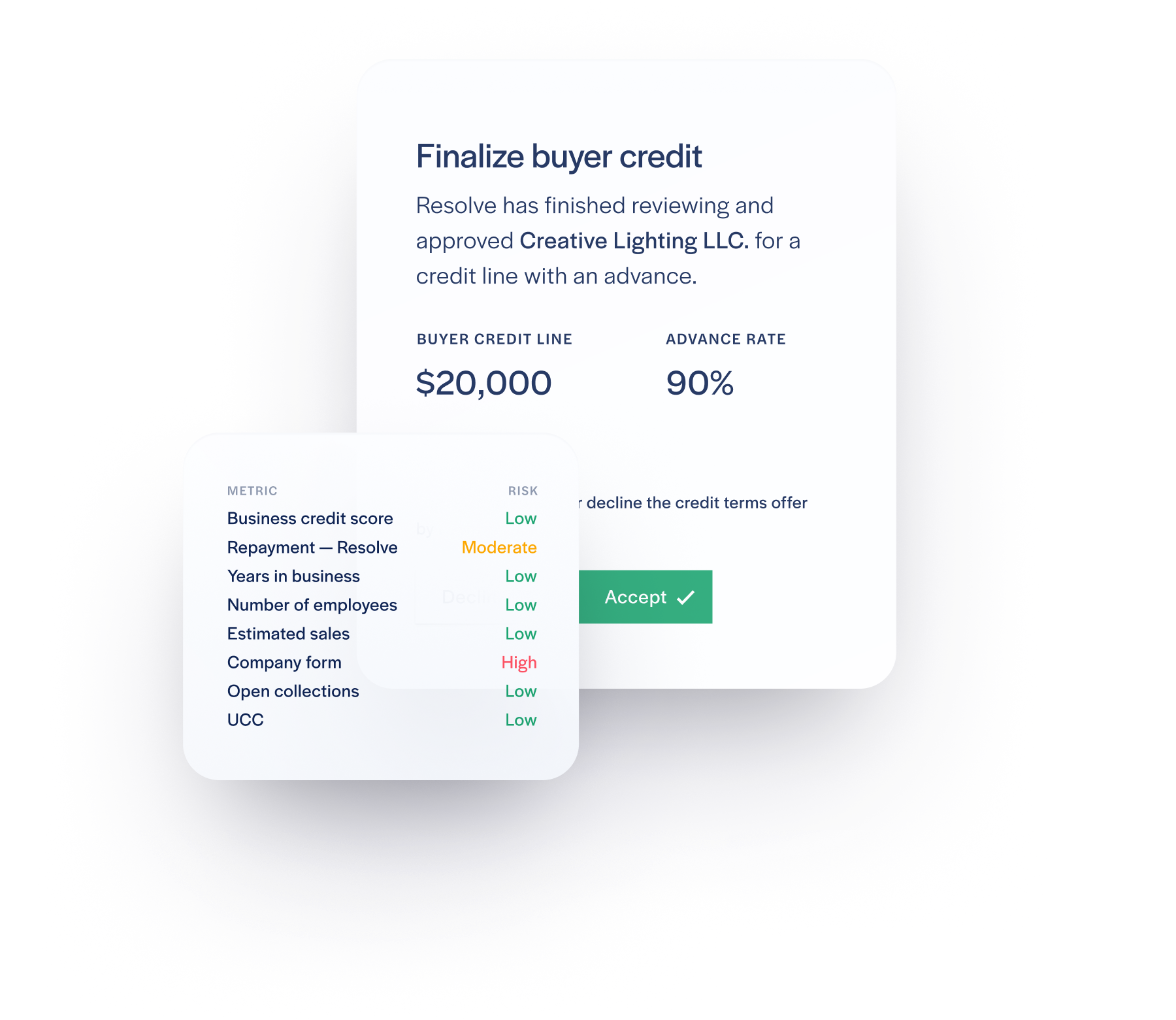

Introducing the Resolve net terms management solution. We understand you want to entice valuable customers by providing relaxed payment terms for bulk purchases. Still, you can't always do this because it is such a hassle trying to check a customer's credit history and credit report.

Further, you may be hesitant to offer such terms to everyone, especially given that, according to a PwC Global Economic Crime and Fraud Survey, companies lost a combined $42 billion to fraud. in 2020 alone.

At Resolve, we do the heavy lifting by taking care of:

- Credit checking

- Invoicing

- Payment processing

- Payment reminders

- Credit line approvals

- AR collections

More importantly, when it comes to cash, we also offer advance cash payments on approved net term invoices. What's more, integrated receivables solutions like Resolve are becoming more and more popular.

Accounts receivable and the cash flow statement

On the other hand, accounts receivables refer to cash due to your business for services or goods delivered but not paid. Put differently, these are the outstanding invoices unpaid by customers.

It's a short-term line of credit extended to regular customers with an obligation to pay within a set date, often 30, 60, 90, or 120 days. Unlike a loan, AR doesn't typically carry interest—it's a trade credit arrangement that helps facilitate B2B transactions. However, while it sits on your balance sheet as a current asset, it doesn't translate into usable cash until the customer actually pays. That gap between recording the sale and receiving the cash is exactly what makes AR so impactful on your cash flow statement.

The effect of account receivables on cash flow

Account receivables are cash to your business and a short-term liability to the customer. Your cash flow considerations will determine how long you can allow a customer to go without paying.

On the balance sheet, the supplier records the short-term credit as current assets, affecting cash flow as accounts payable. Allowing a customer more time before they pay is an account receivable.

For instance, if you make a sale of $10,000 with terms of sale at 50% cash and 50% credit payable within 60 days, record the $5,000 as sales since it is a cash inflow. You will record the balance as an inflow when it is paid.

Here, Resolve can come in handy to enhance your accounts receivable. Did you know that Resolve makes net terms risk-free? We shoulder all the risk as we are the lender.

What's more, we offer up to 90% of customer's invoices, processed within one day. After analyzing a client, we advise you to grant them 30, 60, or 90 days within which to pay us. That way, your business will always have cash flow, whatever your accounts receivable situation.

How AR changes impact the cash flow statement

The relationship between accounts receivable and your CFS boils down to one core rule: when AR increases, operating cash flow decreases, and when AR decreases, operating cash flow increases. The table below breaks down how this works in practice.

| Scenario | AR Increases | AR Decreases |

|---|---|---|

| What it means | More sales were made on credit than cash collected from customers | More cash was collected from customers than new credit sales were generated |

| Impact on CFS | Subtracted from net income (reduces operating cash flow) | Added back to net income (increases operating cash flow) |

| Cash effect | Less cash available for operations, payroll, and growth | More cash available for reinvestment and expenses |

| Possible causes | Rapid sales growth, extended payment terms, slow-paying customers | Improved collections, shorter payment terms, customer prepayments |

| Risk signals | Higher bad debt risk, potential liquidity crunch | Generally positive; verify it's not due to declining sales |

| Example | AR grows from $80K to $130K → subtract $50K from operating cash flow | AR drops from $130K to $90K → add $40K back to operating cash flow |

To put this in a real-world scenario: suppose your business reports $200,000 in net income for the quarter. However, your accounts receivable grew by $50,000 during the same period because you onboarded several new customers on net 60 terms. On the CFS (using the indirect method), you'd start with the $200,000 net income and then subtract the $50,000 AR increase, leaving you with $150,000 in operating cash flow. That $50,000 difference represents revenue you've earned on paper but haven't actually collected yet.

How to record accounts receivable

In the double-entry system of bookkeeping, if you make credit sales, debit accounts receivable—meanwhile, credit cash sales as income.

If you use the accrual concept, that means accounts receivable will increase along with sales, that is to say, they form part of your net profit.

The CFS's starting point is net profit, which increases although there are no cash transactions. This is unacceptable. Therefore, deduct any net profit or indirect sales that do not involve such transactions.

You have to deduct increases in accounts receivables from the net profit to cash used from operations. Here's a simplified example of how the adjustment works. Say your business had net income of $75,000 for the month, depreciation of $5,000, and your AR balance grew by $20,000. Under the indirect method, the operating cash flow calculation would look like this: $75,000 (net income) + $5,000 (depreciation add-back) − $20,000 (AR increase) = $60,000 in net cash from operations. That tells you that while your income statement says $75,000 in profit, you only actually generated $60,000 in cash—because $20,000 is still sitting in unpaid invoices. Keeping an eye on this gap is essential, and it's one reason many B2B businesses turn to outsourced AR management to speed up collections.

The financial statement presentation of accounts receivable

Remember to subtract any increases in accounts receivables from net profit and add any decreases in accounts receivables back to net profit.

When you debit the cash or bank account against accounts receivable, only the accounts receivable entry impacts cash flow. Therefore, make sure to record this movement in your cash flow statement.

First, subtract the current period cash amount in your accounts receivable from the previous period's cash amount. A positive result indicates an increase in accounts receivable, which uses cash and reflects a cash flow decrease by the same amount.

Conversely, a negative result points to a cash flow increase of the same magnitude.

How to reduce AR's drag on your cash flow statement

Four strategies that directly improve the operating cash flow section of your CFS.

1. Tighten credit terms before extending them

Run a business credit check before approving net terms. Approving the wrong buyers inflates AR and increases bad debt risk simultaneously. Resolve's AI credit engine evaluates thousands of buyer data points and delivers decisions in under 24 hours, so your team can say yes faster to the right customers and protect cash flow from the wrong ones.

2. Automate invoicing and follow-up

Every day between invoice issue and payment receipt is a day AR sits on the CFS as a cash drag. Agentic collections compress that gap without adding headcount. Resolve's AI agents run multi-channel follow-up sequences, place autonomous outbound calls at day 14, log outcomes, and escalate disputes, all without manual intervention.

3. Use early payment incentives

2/10 net 30 (a 2% discount for paying within 10 days) converts slow-paying AR into faster cash inflows. The cost is predictable; the cash flow benefit is immediate. Pair this with smart payment method strategies to reduce the friction between invoice and payment.

4. Convert AR into same-day cash with a net terms platform

Resolve advances up to 100% of approved invoice value within one to two business days. Your CFS reflects the advance as a cash inflow immediately, not 30, 60, or 90 days later. And because Resolve assumes the credit risk, a buyer default does not create a bad debt write-off on your CFS either. Calculate your AR ROI to see the cash flow impact.

Key AR metrics that impact cash flow

Understanding the relationship between accounts receivable and your cash flow statement is only half the equation. To actively manage and improve that relationship, you need to track a few critical AR performance metrics. These indicators help you spot collection problems early, benchmark against industry norms, and make smarter decisions about credit policies and B2B payment terms.

Days sales outstanding (DSO)

DSO measures the average number of days it takes your business to collect payment after a sale is made. The formula is: DSO = (Average Accounts Receivable ÷ Total Credit Sales) × Number of Days in Period. For example, if your average AR balance is $100,000 and your total credit sales for the quarter are $300,000, your DSO would be ($100,000 ÷ $300,000) × 90 = 30 days. A rising DSO means customers are taking longer to pay, which directly reduces the operating cash flow on your CFS. A declining DSO indicates your B2B collections process is improving, which frees up cash faster.

Accounts receivable turnover ratio

This ratio tells you how many times per period your business collects its average AR balance. The formula is: AR Turnover Ratio = Net Credit Sales ÷ Average Accounts Receivable. A higher ratio means you're collecting receivables more frequently—turning credit sales into cash faster. For instance, a turnover ratio of 12 means you collect your full AR balance roughly once per month on average. If that ratio drops to 6, it means you're only collecting every two months, signaling that more of your cash is tied up in outstanding AR balances and dragging down your operating cash flow.

Collection effectiveness index (CEI)

CEI measures how effective your team is at collecting receivables within a given period, regardless of how much new credit you've extended. Unlike DSO—which can be skewed by seasonal sales spikes—CEI isolates your actual collection performance. The formula is: CEI = [(Beginning AR + Credit Sales − Ending AR) ÷ (Beginning AR + Credit Sales − Ending Current AR)] × 100. A CEI of 80% or above is generally considered healthy. If it drops below that, it could indicate that your collection efforts need improvement, which will eventually show up as consistently negative working capital adjustments on your cash flow statement. Pairing a strong CEI with smart payment method strategies is one of the most effective ways to keep your operating cash flow healthy.

Frequently asked questions

Is accounts receivable reported on the cash flow statement?

Yes. Accounts receivable appears in the operating activities section of the cash flow statement. It isn't listed as a standalone line item like on the balance sheet. Instead, the change in accounts receivable between periods is shown as an adjustment to net income. An increase in AR is subtracted from net income, while a decrease is added back. This adjustment reconciles the difference between your accrual-based profit and the actual cash your business generated.

Why is an increase in accounts receivable negative on the cash flow statement?

An increase in accounts receivable means your business has earned revenue on paper (through credit sales) but hasn't collected the cash yet. Since the CFS tracks actual cash movement, this uncollected revenue must be subtracted from net income to avoid overstating how much cash the business truly generated. Think of it as money your customers owe you that's still sitting in their bank accounts instead of yours.

Does a decrease in accounts receivable increase cash flow?

Yes. When your accounts receivable balance drops, it means customers have paid their outstanding invoices, converting those receivables into actual cash. On the CFS, this decrease gets added back to net income in the operating activities section because it represents cash that has come into the business. For example, if your AR drops by $30,000 in a quarter, that $30,000 is added to your operating cash flow, reflecting that the money has been collected and is now available for use.

What is a good DSO for my business?

A "good" DSO depends on your industry and the payment terms you offer. As a general benchmark, your DSO should be close to (or ideally lower than) your standard payment terms. If you offer net 30, a DSO of 30–35 days is healthy. If your DSO is significantly higher—say 50 or 60 days when you offer net 30—it indicates that customers are paying late, which is eroding your cash flow. Industries like manufacturing and wholesale distribution often see higher DSOs due to standard net 60 or net 90 terms. Whatever your baseline, the trend over time matters more than any single number.

How do net terms affect the cash flow statement?

When you offer net terms (such as net 30, net 60, or net 90), you're essentially allowing customers to delay payment. This delay increases your accounts receivable balance, which in turn reduces operating cash flow on the CFS. The longer your net terms, the more working capital is tied up in unpaid invoices. This is one of the main reasons B2B businesses use AR financing solutions or net terms management platforms to receive cash advances on outstanding invoices—so they can offer competitive payment terms without sacrificing liquidity.

What is the difference between accounts receivable and accounts payable on the cash flow statement?

Accounts receivable and accounts payable have opposite effects on cash flow. An increase in AR reduces cash flow (because you've extended credit but haven't collected cash), while an increase in AP increases cash flow (because you've received goods or services but haven't paid for them yet). Both appear in the operating activities section of the CFS. Together, they are key components of your working capital and directly determine how much cash you have available day-to-day.

Can you have high revenue but low cash flow because of accounts receivable?

Absolutely—and it happens more often than you might expect. If a business is growing rapidly and extending credit terms to new customers, revenue on the income statement can look excellent while the CFS tells a very different story. A company might report $500,000 in quarterly revenue but have $200,000 of that tied up in unpaid AR, leaving far less actual cash available for payroll, inventory, and operating expenses. This is often referred to as the "profitable but cash-poor" trap, and it's one of the most common cash flow challenges facing growing B2B businesses.

Ready to break the shackles of risky net terms while improving your cash flow and accounts receivables? Why not try Resolve net terms financing for B2B businesses? We even offer free business credit check as part of the free trial offer. Get a demo today.

{kind=link}